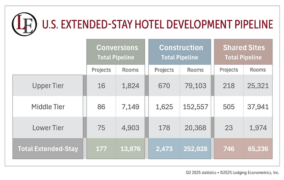

Extended-stay hotels represent a dominant force in the U.S. hotel development landscape, maintaining their position as the largest segment of the construction pipeline. As of the second quarter of 2025, extended-stay brands comprise 2,473 projects totaling 252,028 rooms—accounting for 39% of all projects and 34% of all rooms currently in the pipeline. Additionally, 177 properties are undergoing conversion to extended-stay brands, contributing another 13,876 rooms to the pipeline. These conversions include a mix of existing extended-stay hotels transitioning between brands and traditional hotels being repositioned as extended-stay properties.

This segment’s strength is evident across all development phases. Currently under construction, extended-stay hotels represent 420 projects with 44,770 rooms, constituting 38% of the 1,120 active construction projects and 32% of total rooms being built. Looking ahead, 976 extended-stay projects encompassing 101,853 rooms are scheduled to break ground within the next twelve months, representing 43% of the 2,263 planned projects and 39% of the 260,052 rooms set to begin construction. In the early planning stages, an additional 1,077 extended-stay projects with 105,405 rooms account for 37% of the 2,897 projects and 31% of the 338,208 rooms in preliminary development phases.

A notable component of this development activity involves shared site projects, where extended-stay hotels are part of larger, multi-hotel developments. These collaborative developments account for 746 projects totaling 65,236 rooms within the extended-stay pipeline, demonstrating how developers are increasingly integrating extended-stay hotels into comprehensive hospitality complexes that can serve diverse traveler segments within a single location.

Extended-stay brands are strategically positioned within upper, middle and lower tiers to capture various customer segments and price points. Major franchise companies have recognized this opportunity by building substantial extended-stay portfolios, with Marriott International, Hilton, IHG Hotels & Resorts, Hyatt Hotels, Wyndham Hotels & Resorts and Choice Hotels collectively operating 20 extended-stay brands across the various tiers, creating a comprehensive approach to meet varying guest needs and preferences.

The upper tier commands 670 projects encompassing 79,103 rooms, a substantial offering for a segment consisting of only five brands, all of which belong to the above-mentioned franchise companies. The middle tier represents the largest opportunity, featuring 25 brands that account for 1,625 projects and 152,557 rooms in the pipeline—with these six franchise companies controlling 11 of these brands and capturing the majority of this segment’s growth. Meanwhile, the lower tier, though smaller with 12 brands representing 178 projects and 20,368 rooms, still attracts investment from four brands operated by these same hospitality companies above, demonstrating their commitment to comprehensive coverage across all price points

With a substantial pipeline spanning all tiers, the extended-stay segment is projected to maintain strong momentum over the next three years. The format’s appeal to developers lies in its ability to attract diverse guest segments, from corporate travelers and government personnel on extended assignments to construction crews, remote workers, relocating families, and leisure guests seeking the conveniences that extended-stay properties offer. By combining home-like amenities with hotel services, extended-stay properties generate consistent revenue streams and deliver attractive returns on investment that continue to drive development activity.

Through 2027, LE projects robust expansion in the extended-stay sector, with 1,018 new hotels anticipated to open and contribute 105,051 rooms to the nation’s operating inventory. The growth trajectory shows steady acceleration over the three-year period. In 2025, the sector is expected to welcome 293 new properties encompassing 30,341 rooms, representing a 5% growth rate. This momentum builds in 2026 with the addition of 340 hotels and 34,909 rooms, pushing the growth rate to 5.5%. The expansion peaks in 2027, when 385 new extended-stay properties are forecast to open with 39,801 rooms, achieving a 5.9% growth rate and marking the strongest year of inventory expansion in the forecast period.

Choose Lodging Econometrics (LE) to unlock the full potential of extended-stay’s record-breaking development cycle. We can provide you with project-level details, developer and project team member contact information, market specifics, and more. Contact +1 603.431.8740, ext 0025 or info@lodgingeconometrics.com.

The post Extended-stay hotels set for expansion appeared first on hotelbusiness.com.

Source: hotelbusiness.com